They never hand over complete control over yields to the market.

Written by Wolf Richter of Wolf Street.

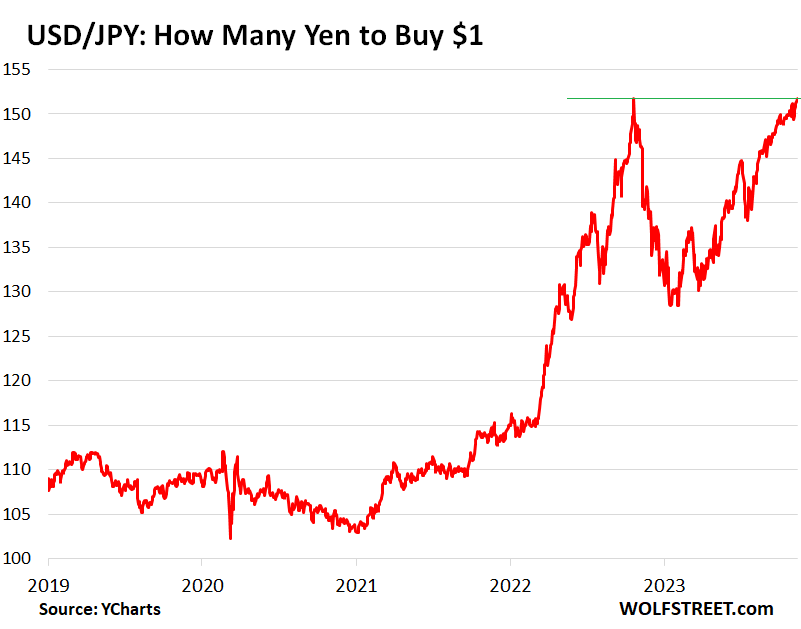

The yen fell to 151.92 yen to the dollar earlier today, just shy of its intraday low in October 2022, then rebounded sharply to 151.22 yen, but has now fallen again to 151.72 yen.

Finance Minister Shunichi Suzuki said today that the government will closely monitor the situation and respond appropriately. That was the answer. The graph shows increments over time.

That USD/JPY 152 was today’s trigger mark. There were approximately $1.25 billion in option contracts expiring today at 10 a.m. ET, with a strike price of 152, according to the company. Reuters. Another $2.2 billion expires on Wednesday.

And Mark Chandler, chief market strategist at Bannockburn Global Forex, said the yen’s sharp and short-lived rebound against the dollar earlier today was due to option expirations, not BOJ intervention. told Reuters.

The yen’s sharp decline and volatility began in September 2021, when the Federal Reserve announced it would begin tightening in response to inflation starting to pick up steam. Until then, the yen exchange rate had fluctuated at around 110 yen to the dollar, and had remained in that range for many years.

By October 2022, with the yen plummeting uncontrollably towards the 150 yen level and threatening to overshoot the yen exchange rate, the Treasury and Bank of Japan duo decided to sell dollar-denominated securities to prevent the yen from depreciating. He orchestrated a huge wave of selling and buying of the yen. It worked, and the yen eventually rebounded somewhat. However, it didn’t last long and things went back to normal, but this time the two of them just kept moving.

Adios, international purchasing power.

At an exchange rate of 151 yen to the dollar, starting in 2021, Japanese consumers and businesses will lose approximately 27% of their purchasing power when it comes to imported goods, including food and energy products, as well as foreign acquisitions and overseas travel. It means something. As a result, Japanese consumers and businesses are looking to shift spending to Japan and end up paying much more for imported goods. That’s the purpose.

The Bank of Japan, the last central bank still clinging to negative policy rates, is currently inching away from negative policy rates and is pursuing a well-documented strategy of boosting inflation. , governments are also supporting these inflationary efforts with subsidies and stimulus spending. .

And while Japanese authorities now appear to be aiming for a permanently weaker yen, perhaps to the 150 yen level or below, they are not allowed to communicate such plans because it would be considered currency manipulation. So everything is a little delicate.

However, the situation must remain under the control of the government and the Bank of Japan. There should be no currency confusion. And when things go too fast, they intervene. But when things go slowly and methodically to the same place, they let it go.

Snail-like withdrawal from NIRP and yield curve control.

Back in 2016, the Bank of Japan followed the foolish actions of Europe and lowered the one-month policy rate to -0.1%, where it remains today. However, it has hinted that it may withdraw from the negative interest rate policy (NIRP).

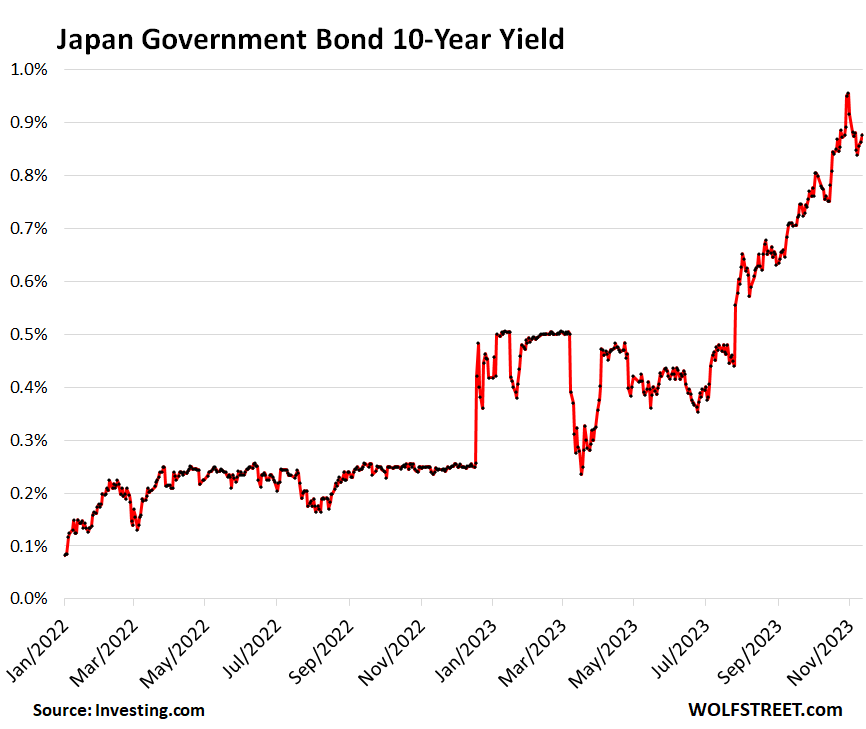

In preparation to avoid a yield inversion, yield curve control has been gradually eased. For years, through yield curve control, the Bank of Japan has fixed the 10-year yield first below 0.10% and then below 0.25% to protect that level by purchasing Japanese government bonds (JGBs).

They then raised the cap on the 10-year bond yield to 0.5% on December 20, 2022, which caused all sorts of confusion as seen in the graph below.

This year, the Bank of Japan raised the cap to 1.0%, then announced in October that the 1.0% cap was no longer a fixed cap, but a gentle “ceiling,” and 10-year bond yields were zigzagging toward it. ing. Level, currently 0.88%:

Keep the yield curve steep while tightening.

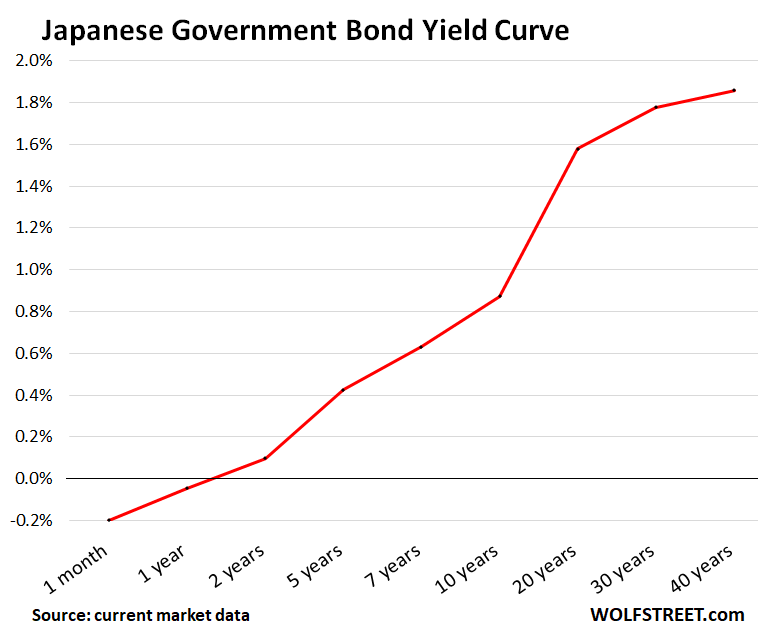

By allowing long-term interest rates to rise while still keeping short-term policy rates negative, an inversion of the yield curve was prevented. This phenomenon occurred in the United States and produced 18 months of unrelenting recession-fueling.

In contrast to the US yield curve, Japan’s yield curve, although controlled, is quite steep, with short-term interest rates of -0.2% (below the Bank of Japan’s policy rate) and one-year bond yields of – The yield on 2-year bonds is 0.10%, and the yield on 5-year bonds is 0.43%. The 10-year yield is 0.88%, the 20-year yield is 1.58%, the 30-year yield is 1.78%, and the 40-year yield is 1.86%.

There is no love for the market.

Japanese authorities have never believed in a true market for government bonds. The government and the Bank of Japan will never allow the market to move Japanese government bond yields as they please. They are always more or less controlled. The only question is how much control they have.

The Bank of Japan owns more than half of the world’s government bonds, placing a huge burden on major government agencies. Other Japanese institutions that the government and the Bank of Japan can rely on have an even bigger pile. There is very little market left.

Moody’s this weekend affirmed the U.S. credit rating at triple-A, and only lowered the outlook on that triple-A rating to negative (meaning it may lower the rating in the future), but it has long since revised Japan’s credit rating. has been lowered to A1. , four notches lower than the US rating (My Bond Credit Rating Cheat Sheet). And since there is no free market for Japanese government bonds, it is just a decoration and not a problem.

The entire situation, including the pace of destruction of the yen exchange rate, the pace of inflation, the pace of rise in government bond yields, and the yield curve, must be brought under the control of the government and the Bank of Japan. There should be no currency confusion or yield confusion. And when things move too quickly, the authorities intervene. However, we are seeing a shift in policy toward a weaker yen and higher yields.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how:

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()